The US’s Critical Mineral Offensive Strategy: How Can Europe Step Up?

As Organization for Economic Co-operation and Development (OECD) economies are confronted with mounting threats to critical raw materials (CRM) supplies, resolute interventionist policies are needed to build resilient value chains.

Critical Minerals: a strategic priority for the US

From 2021 to February 2026, the United States (US) deployed an estimated 40 billion euros (EUR) in support of CRM projects, approximately eight times the funds allocated by the European Union (EU).

The Trump administration has reinforced the US strategic approach: new funds were created by the One Big Beautiful Bill Act (OBBBA) enacted in July 2025, the Department of War (DoW) took a central role, the “Vault” strategic stockpile project was announced. The American approach is offensive and swift, as demonstrated by bilateral deals made with Ukraine and the Democratic Republic of Congo.

Increased support by the Trump II administration

The OBBBA legislation included key provisions for critical minerals, such as the establishment of an Industrial Base Fund (USD 5 billion), USD 2 billion for the National Defense Stockpile Transaction Fund, and a Critical Minerals Loan Program (up to USD 500 million per project). Conversely, the OBBBA reduced substantial portions of the Inflation Reduction Act (IRA), including tax credits that encouraged electric vehicle (EV) purchases. An example is the cancellation of the 30D tax credit effective September 30, 2025.

In the effort to secure CRM value chains, the new administration is giving an increasing role to the DoW. Since January 2025, at least ten CRM companies have been supported by the DoW through the Defense Production Act (DPA). Support via the DPA for CRM projects has resulted in USD 550.4 million (M) in aid for fiscal year (FY) 2025, compared to USD 209.2 M for FY 2024, and USD 313.6 M for FY 2023. This practice has thus grown with the second Trump administration, but was already in place under Joe Biden and is not new.

Probably the most significant support action taken by the DoW is the deal finalized in July 2025 with rare-earth magnet producer MP Materials. Through this deal, the DoW invested USD 400 M in MP Materials, while the Office of Strategic Capital provided the company with a USD 150 M loan to improve its heavy rare-earth separation capabilities at the Mountain Pass site in California. Additionally, a 10-year agreement was signed, establishing a minimum price of USD 110 per kilogram for MP Materials’ NdPr (neodymium, praseodymium) products stored or sold. The DoW also committed to purchasing 100% of the magnets produced at the planned new “10X Facility” for ten years.

An agile and swift approach

Having held significant importance during the previous tenure, especially through the Bipartisan Infrastructure Law (BIL) and the IRA, the Department of Energy (DoE) has not lost its role, even though it is less central now. Some important IRA tax credits have been preserved, and several new funds were added in August 2025, totaling around USD 1.1 billion (bn). The US Development Finance Corporation (DFC) and the Export-Import Bank (EXIM) also play a key role in this strategy, notably through loans and letters of interest.

The US has approached CRMs as a strategic mobilization challenge, deploying private finance, targeted federal support and a diverse set of instruments. Private capital has been central, with the DFC and EXIM derisking early-stage projects and accelerating investment. Federal support has been highly targeted, focusing on specific bottlenecks such as rare earth separation and magnet manufacturing.

Moreover, the US industrial strategy on CRMs is supported by active mineral diplomacy. According to the Department of State, since Donald Trump’s return to the White House, the US has signed 21 bilateral critical frameworks or memorandums of understanding (MoUs) with third countries, and has finalized negotiations on such agreements with seventeen other nations.

What lessons for Europe?

The main lesson for Europe is straightforward but uncomfortable: credibility requires deployable capital and the institutions to use it. Announcing strategic projects without the public money to finance them is not taken seriously by partners or competitors. Europe lacks dedicated, ring-fenced funds for CRM projects, as well as the institutional vehicles capable of deploying capital at speed and scale. There is no European equivalent to DFC or EXIM, no instrument able to take equity stakes or anchor investment funds as the US has with TechMet or Orion. Nor has Europe mobilized its own downstream industries—clean tech manufacturers, digital firms, defense primes—to invest directly in the CRM value chain projects on which their long-term resilience depends.

The EU must adopt a complementary approach across its various sectors related to metals, such as defense, energy, and electronics. Funds allocated to European rearmament efforts should include metals, and certain European defense funds can be used for this purpose. It is also crucial that the future CRM Centre has a dedicated budget within the next Multiannual Financial Framework (MFF). Beyond traditional actions, the EU should rethink its model by employing less-used or unused methods, such as equity investments. This also involves streamlining investment decision processes.

The Power of Demand-Side Measures

Crucially, US policy includes hard obligations on downstream users. “Buy America” provisions create structural preferences for domestic or Free Trade Agreement (FTA) partner content, while the National Defense Authorization Act (NDAA) bars companies from US defense procurement if any part of their supply chain for certain defense-relevant minerals involves a foreign entity of concern. This combination of targeted support and mandatory compliance has created powerful demand signals for non-Chinese supply.

For Europe, the implication is clear: diversification cannot rely solely on subsidies and regulatory frameworks.

Opportunities for a More Assertive EU Approach

The Industrial Accelerator Act of March 4, 2026, opens the door to more assertive use of public procurement and state aid. Embedding a calibrated “Buy European” or “trusted origin” requirement into that framework would align incentives for downstream manufacturers.

The European Commission’s proposal, published in early March, does not include precursor cathode active materials (PCAMs) among the battery components subject to the origin requirements of Article 34. However, PCAMs are the main missing link in the current European battery value chain. This gap is harmful both in terms of sovereignty and for economic reasons, as this value chain requires an integrated approach and simultaneous development of its various stages to enable the emergence of offtake agreements, etc.

The planned revision of EU defense procurement rules later in 2026 offers an opportunity to introduce a European analogue to the NDAA’s foreign entity-of-concern logic, conditioning access to defense contracts on the progressive elimination of high-risk critical mineral and component suppliers.

There is currently an ongoing EU–US discussion about minimum price mechanisms or price bands to counteract predatory pricing and market volatility. Designing such tools will be very challenging. The EU must also determine its level of involvement in initiatives proposed by the US, such as the FORGE initiative announced in early February. While international cooperation seems vital for securing supply chains, the EU must also be careful to avoid partnerships where governance is solely controlled by Washington and that might oppose its interests.

Another issue is the consolidation of standards-based markets. Europe has a comparative advantage in environmental, social and governance (ESG) criteria, traceability, product passports and permitting frameworks. If interoperable with US and Japanese systems, such standards could create a global market segment that rewards transparency and sustainability. But they must be designed in a way that producer countries see as enabling value addition rather than restricting market access.

Europe must also strengthen its foreign investment screening in critical minerals. The US has used the Committee on Foreign Investment in the US (CFIUS) process aggressively to block Chinese acquisitions in sensitive sectors. Europe’s mechanisms remain fragmented and uneven. A more coordinated approach focused on processing, refining and strategic assets—while setting conditions for inward investment—would reduce vulnerabilities without undermining openness.

Titre Edito

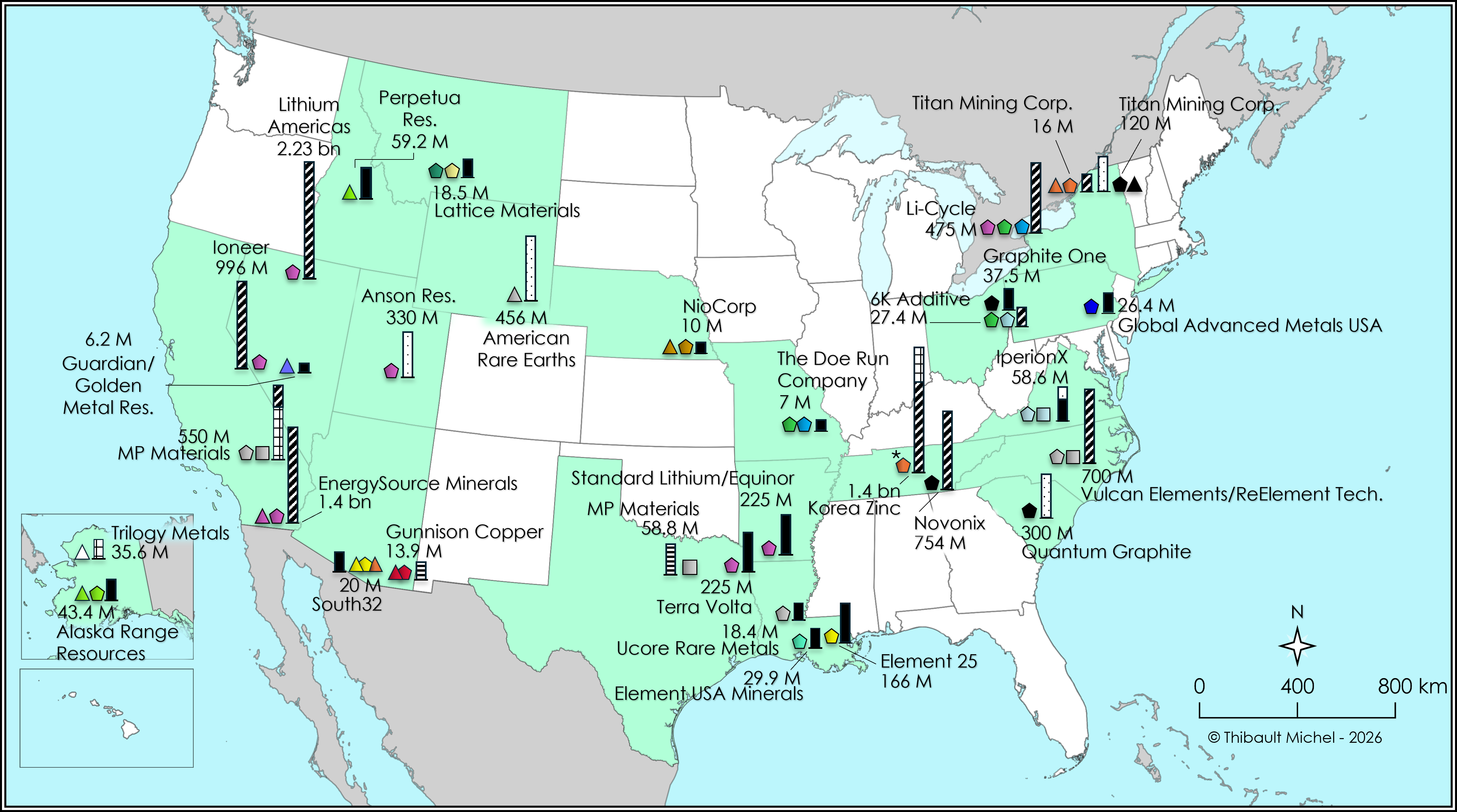

Federal direct announcements of support for domestic CRM projects in 2024 and 2025 (in USD)

Federal direct announcements of support for domestic CRM projects in 2024 and 2025 (in USD)

Titre Edito

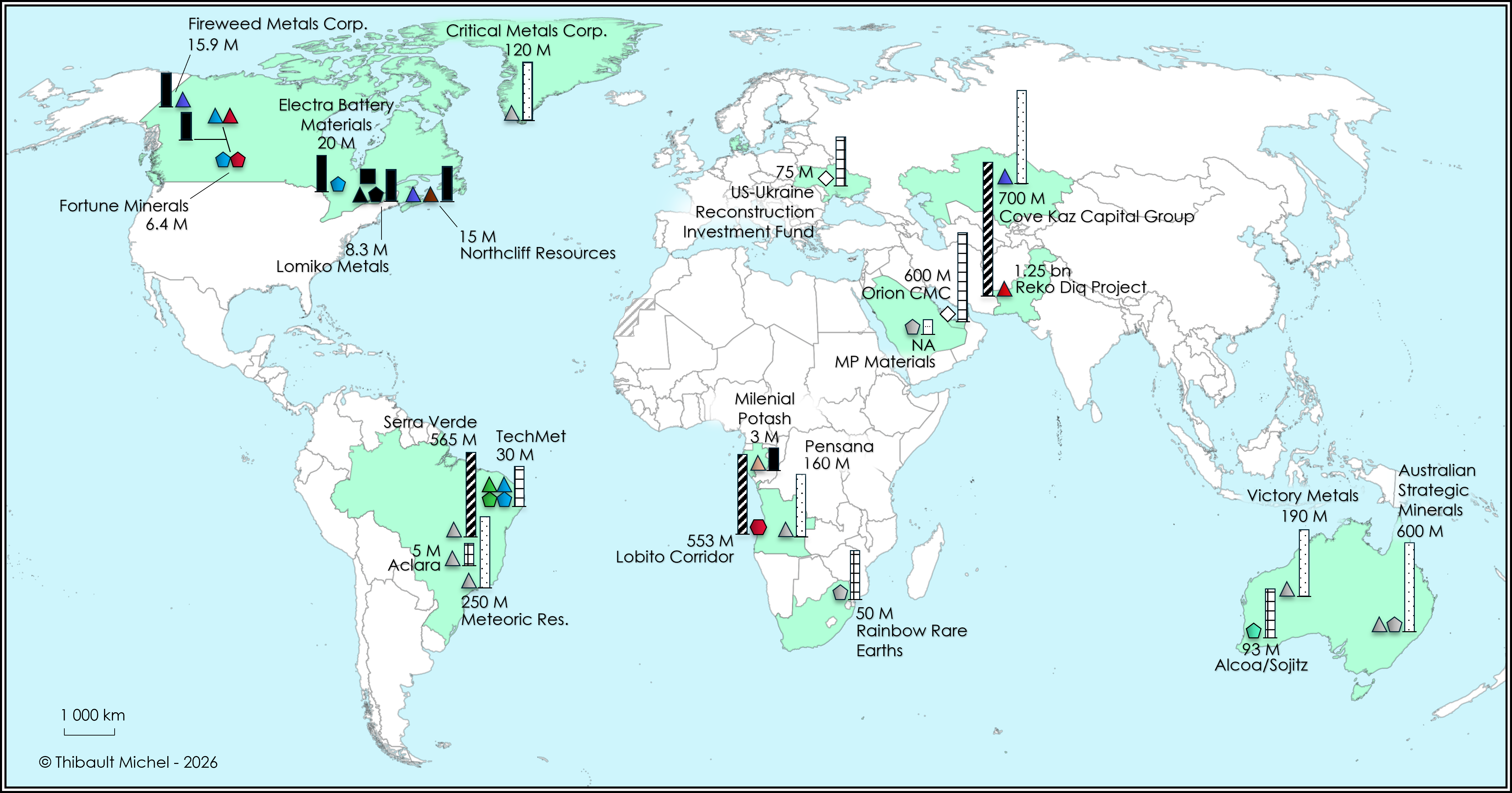

Federal direct announcements of support for CRM projects overseas in 2024 and 2025 (in USD)

Federal direct announcements of support for CRM projects overseas in 2024 and 2025 (in USD)

Available in:

Themes and regions

ISBN / ISSN

Share

Download the full analysis

This page contains only a summary of our work. If you would like to have access to all the information from our research on the subject, you can download the full version in PDF format.

The US’s Critical Mineral Offensive Strategy: How Can Europe Step Up?

Author(s)

Thibault MICHEL

Research Fellow, Center for Energy & Climate, Ifri

Related centers and programs

Discover our other research centers and programs

Center for Energy & Climate

Ifri's Energy and Climate Center carries out activities and research on the geopolitical and geoeconomic issues of energy transitions such as energy security, competitiveness, control of value chains, and acceptability. Specialized in the study of European energy/climate policies as well as energy markets in Europe and around the world, its work also focuses on the energy and climate strategies of major powers such as the United States, China or India. It offers recognized expertise, enriched by international collaborations and events, particularly in Paris and Brussels.

Find out more

Discover all our analyses

How to Make European e-SAF Production under RefuelEU Aviation Fly?

Three and a half years before the scheduled entry into force of the European regulation ReFuelEU Aviation (RFEUA), which requires aviation fuel suppliers at Union airports to offer a sustainable synthetic alternative (e-SAF), no sizeable commercial production unit (greater than 10,000 tons per year) is active within Europe yet, nor has it even passed the Final Investment Decision (FID). Is a major step in the European Union (EU) plans for decarbonizing air transport at risk of not happening, or at least being postponed for several years? Is Europe losing its bet to create a market for e-SAF? Under what conditions can this bet still be won? Could sovereignty and energy security preoccupations unlock necessary public support and help to overcome economic, financial, logistical or administrative obstacles?

The European Biomethane Sector at a Critical Juncture: Stronger Policy Alignment Will Matter

The European biomethane sector is at a critical juncture.

Europe’s Power Grid Challenge: A Make-or-Break for Accelerating Electrification

In April 2023, The Economist published an article pointing to the vast amounts of electricity infrastructure needed to reach energy transition goals.

Germany Maintains Its Single Electricity Price Zone: Implications

In December 2025, Germany refused to split its bidding zone despite recommendations from ENTSO-E, in order to preserve its federal unity, market liquidity, and the competitiveness of its industry, at the cost of persistent North-South imbalances.